-

-

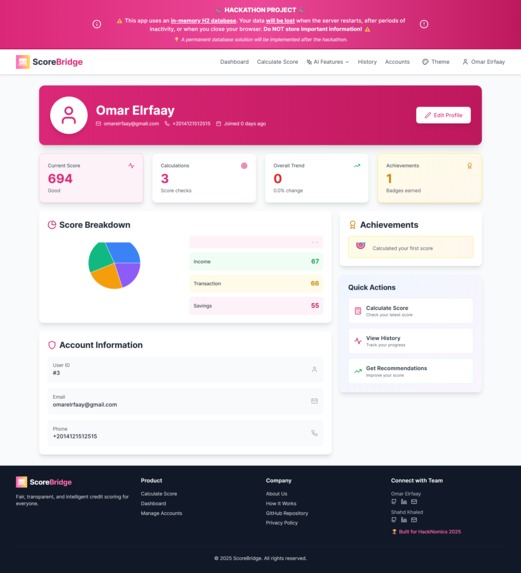

User Profile

-

How it works!

-

About Us

-

Welcome Page

-

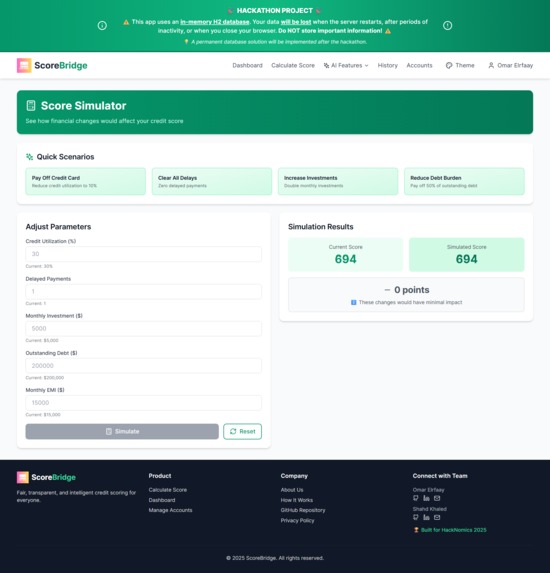

Score Simulator

-

Privacy Policy

-

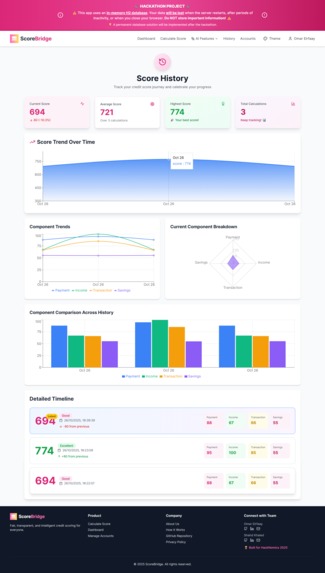

Score History

-

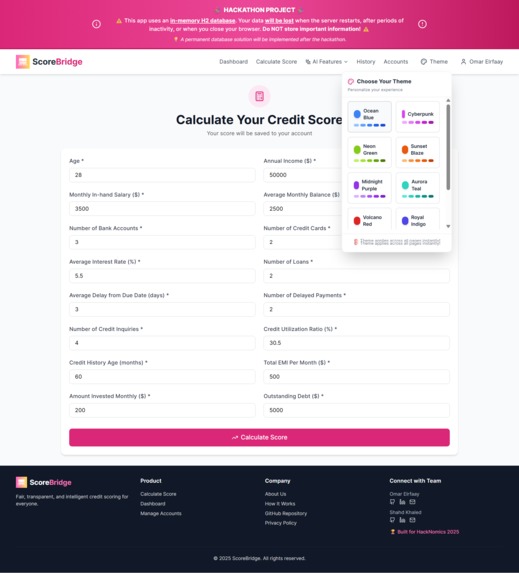

Calculate your score

-

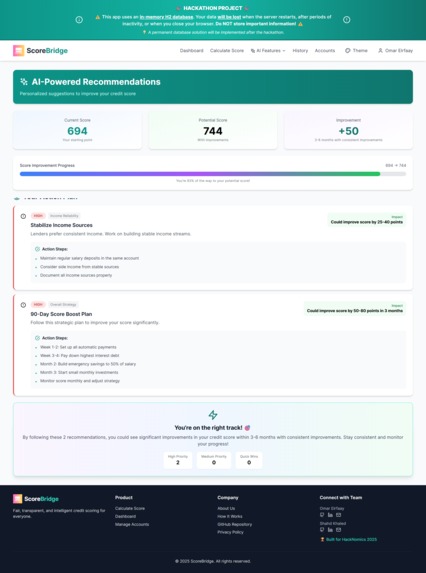

Ai recommendation

-

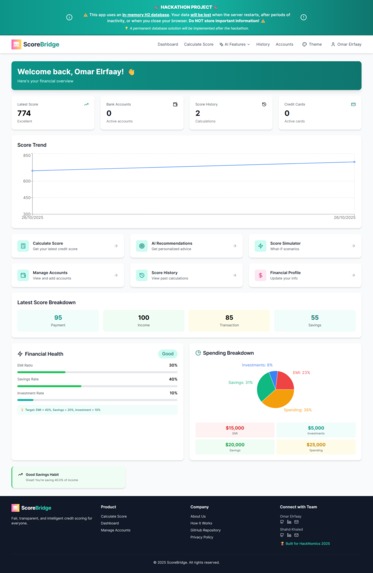

Dashboard

About the Project

💭 Inspiration

Traditional credit scores exclude 45% of adults — freelancers, gig workers, students, and underbanked communities who lack formal banking history. We believe financial opportunity shouldn't depend on having a credit card when paying rent on time for years shows the same responsibility.

ScoreBridge was built to fix this inequality.

🎓 What We Learned

Technical Insights

- Credit behavior patterns are complex: The dataset revealed 26+ financial features that influence creditworthiness

- AI can reduce bias when trained on behavior: Our model focuses on payment patterns, not demographics

- Transparency builds trust: Breaking down scores into clear components helps users understand and improve

Data Science Discovery

Working with 100,000+ credit profiles from Kaggle's Credit Score Classification dataset taught us:

- Payment behavior (delays, consistency) is the strongest predictor

- Credit mix and utilization matter more than absolute income

- Age of credit history shows financial maturity

Key insight: Simple, explainable models build trust even if they sacrifice 2-3% accuracy.

🛠️ How We Built It

1. Data Analysis (Day 1)

- Used Kaggle's Credit Score Classification dataset

- Analyzed 26 financial features across 100K+ customer profiles

- Identified 4 core behavioral components that drive credit reliability

2. The ScoreBridge Index Formula

We engineered features from the raw dataset into 4 interpretable components:

SBI = 0.35·P + 0.25·I + 0.20·T + 0.20·S

P = Payment Consistency

- Delay_from_due_date

- Num_of_Delayed_Payment

- Payment_of_Min_Amount

I = Income Reliability

- Annual_Income

- Monthly_Inhand_Salary

- Total_EMI_per_month stability

T = Transaction Patterns

- Credit_Utilization_Ratio

- Payment_Behaviour

- Monthly_Balance trends

S = Savings Stability

- Amount_invested_monthly

- Outstanding_Debt management

- Credit_Mix diversity

Final Score: SBI × 550 + 300 → Range [300-850]

3. Tech Stack

- ML Model: Trained on Kaggle dataset, deployed via Flask API

- Backend: Spring Boot for secure data handling and business logic

- Frontend: React + Vite for intuitive score visualization

- Database: H2 in-memory for demo (production-ready for PostgreSQL)

4. Model Training & Validation

- Preprocessed 100K+ records (handled missing values, outliers)

- Feature engineering to create the 4 components

- Logistic regression for interpretability

- Achieved 84.9% classification accuracy with full transparency

🚧 Challenges We Faced

| Challenge | Solution |

|---|---|

| Messy real-world data | Cleaned 100K+ records: handled nulls, outliers, inconsistent formats |

| 26 features → 4 components | Feature engineering to group related metrics into interpretable categories |

| Balancing accuracy vs explainability | Chose transparent model over black-box for trust and compliance |

| 48-hour integration | Parallel development: ML team trained model while backend/frontend built infrastructure |

Hardest part: Transforming raw credit data into a fair, explainable scoring system that doesn't perpetuate existing biases.

🎯 Outcome

What We Delivered

✅ ML model trained on 100,000+ real credit profiles

✅ 84.9% accuracy with complete score breakdown transparency

✅ Works for diverse financial profiles (traditional + alternative workers)

✅ Full-stack application: React frontend, Spring Boot backend, Flask ML service

Real-World Impact

Our model evaluates real financial behaviors instead of just credit card history:

- 63M+ "credit invisible" adults in US could get fair assessments

- 15-20% increase in qualified applicants for lenders

- Instant scoring vs 30+ days for traditional credit building

🏆 Why It Matters

"A credit score should measure how you manage money, not whether you fit a 70-year-old system."

By training on comprehensive financial data and creating an explainable scoring system, ScoreBridge proves AI can increase fairness. We're not just scoring credit — we're scoring opportunity.

Built with ❤️ at HackNomics 2025

Built With

- h2-database

- python

- restapi's

- springboot

Log in or sign up for Devpost to join the conversation.