-

-

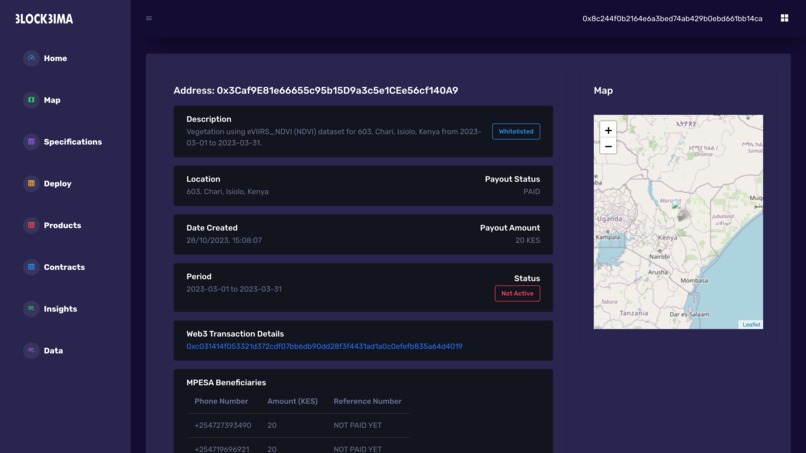

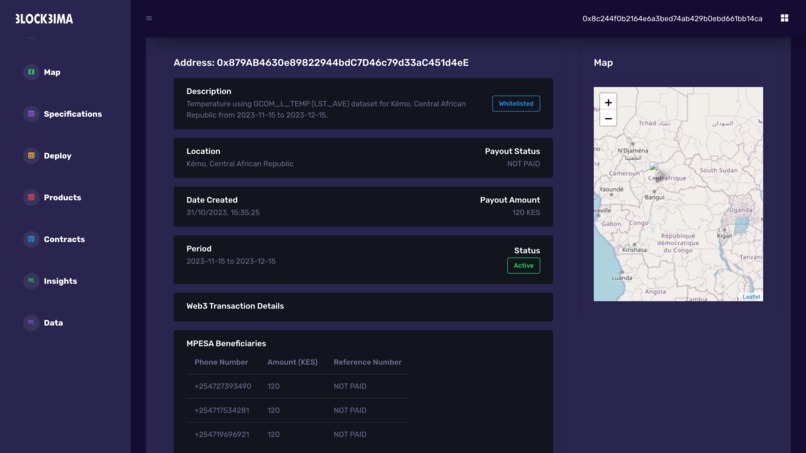

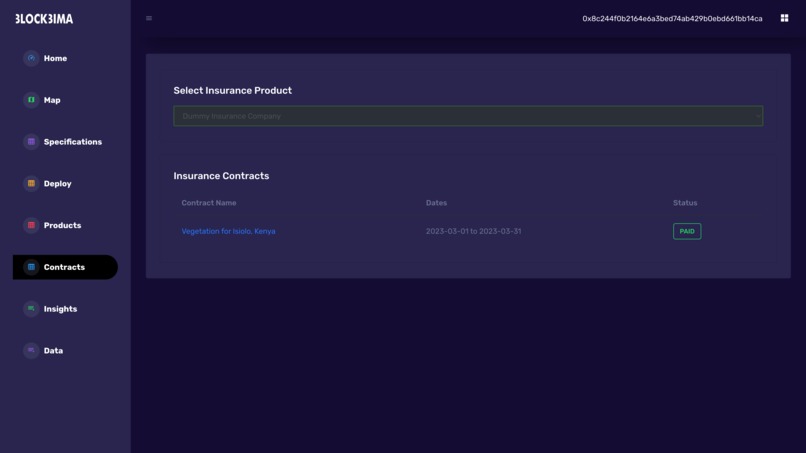

Page showing the details of a specific insurance contract

-

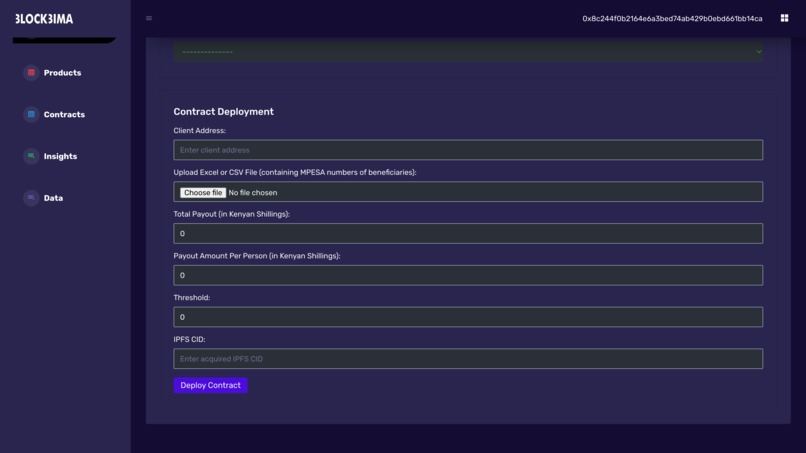

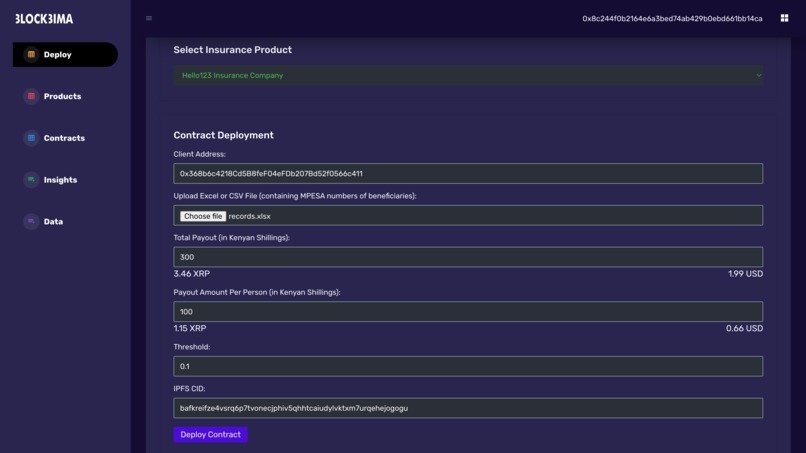

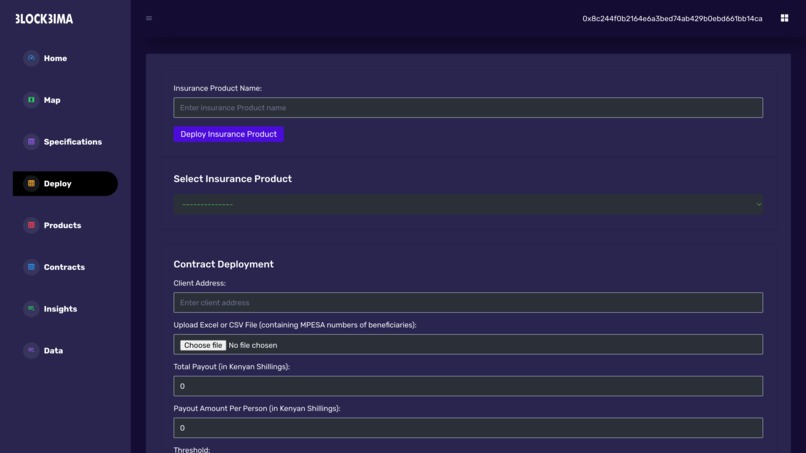

Interface for deploying specific insurance contracts

-

Interface for loading details of the beneficiaries for MPESA payments

-

-

-

-

-

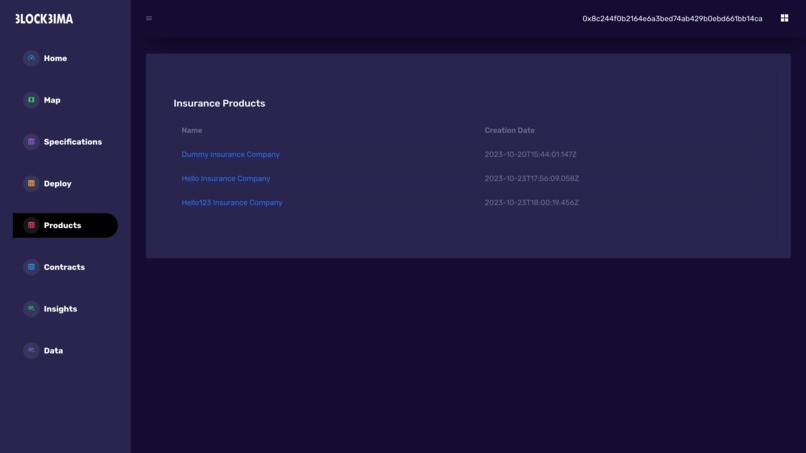

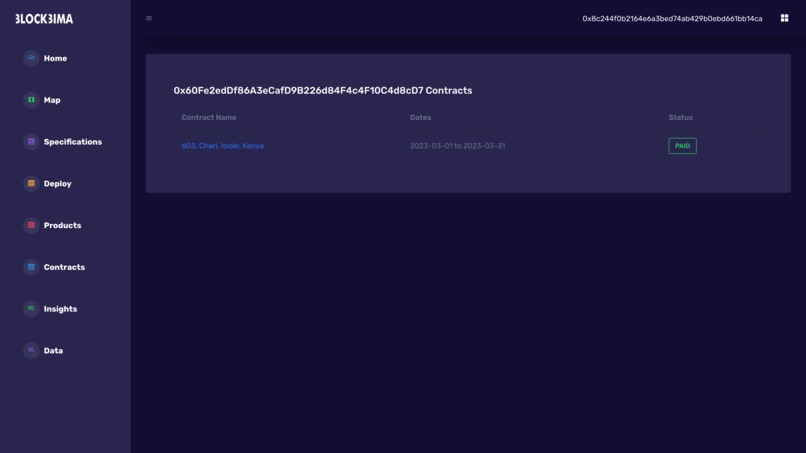

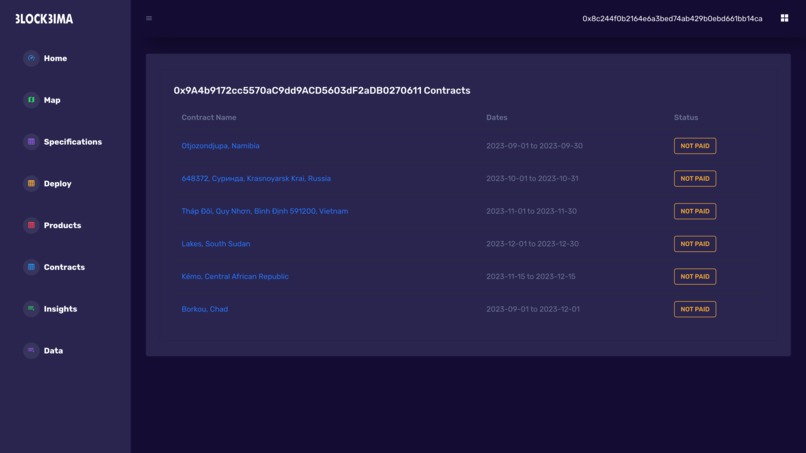

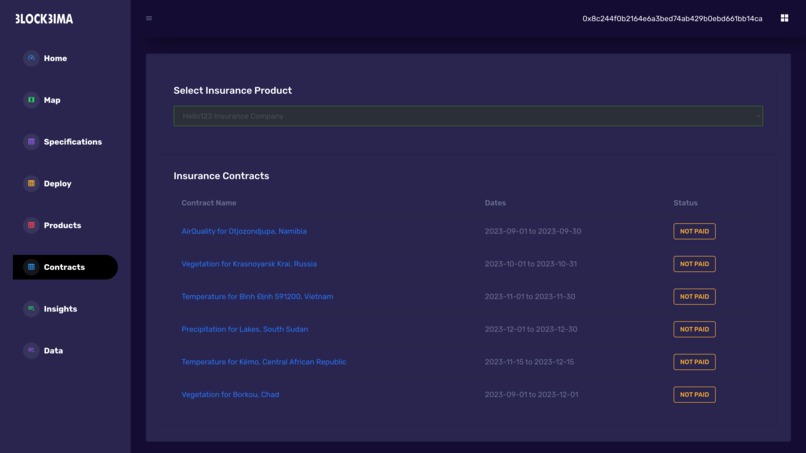

List of individual insurance contracts under a product

-

-

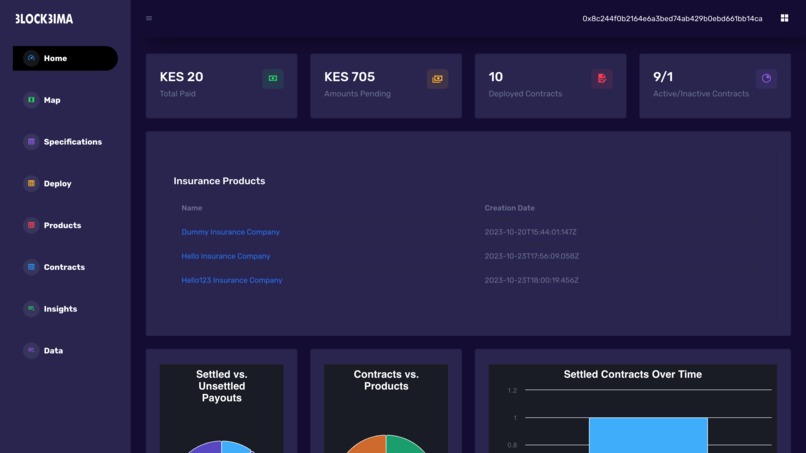

Dashboard for high level overview of user account

-

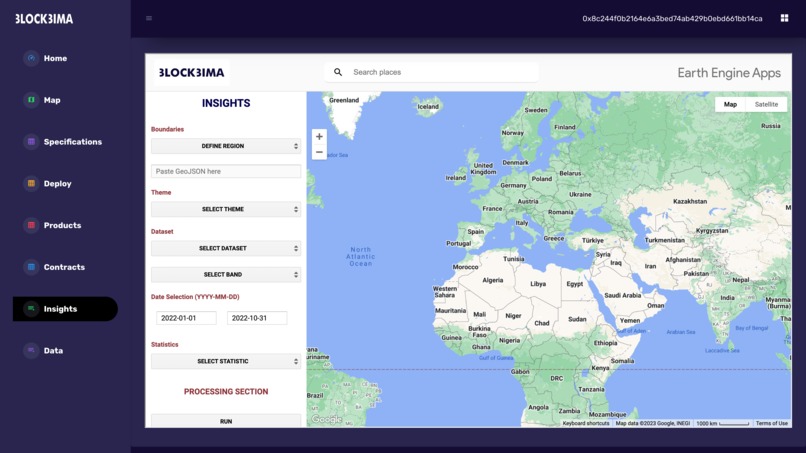

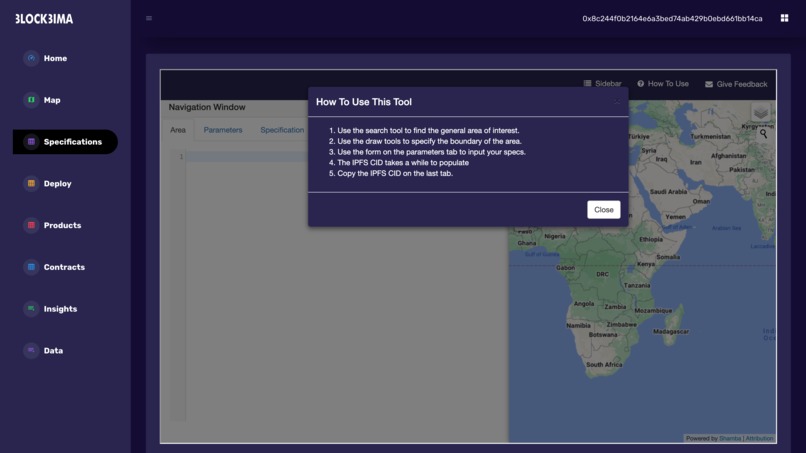

Tool for actuarials to use to find data thresholds and create new insurance products

-

-

Interface for deploying new insurane products

-

Tool for creating the specifications of an insurance contract

-

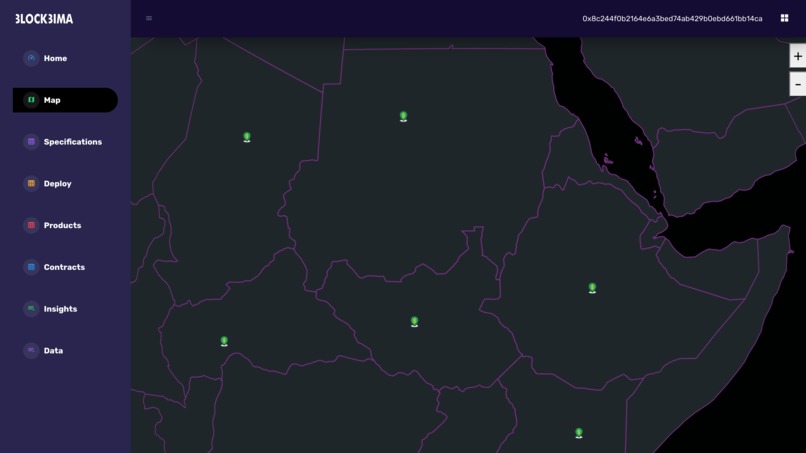

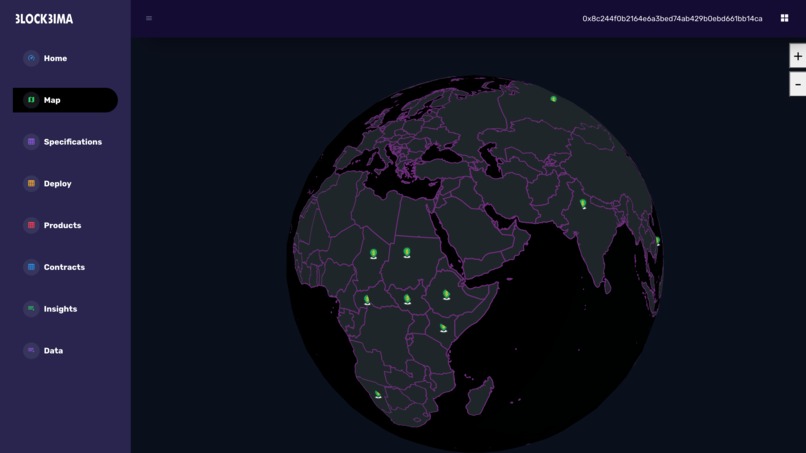

Interactive map spatially showing deployed contracts

-

Inspiration

From 2016 to 2022, the Horn of Africa faced its most extreme drought in 40 years. This precipitated mass displacement, communal conflict, and refugee crises as more than 36 million people were threatened by famine. These are the victims of climate change, and for them, climate insurance is a matter of life and death. Unfortunately, the most climate-vulnerable populations often cannot afford insurance. Traditional insurance is inefficient and thus costly for the vast majority. New solutions are needed to make insurance more efficient and thus financially accessible. This is one area where web3 and CBDCs can have an outsize impact. We were inspired to build this solution to help people from all parts of the world who are facing climate crises in the form of droughts, floods, wildfires, and other risks for which they need to be insured.

What it does

Our solution taps into the power of satellite imagery, geospatial science, machine learning, data oracles, smart contracts, and CBDCs to create an automated form of insurance.

This allows insurance contracts to be deployed on the blockchain using CBDCs on the web3 side of the solution.

A data oracle driven by satellite data reports on-chain the ecological state at the maturity of the insurance contract.

The oracle gets up to date data from NASA and ESA among other satellite providers. This remote sensing data is ingested by the oracle, analysed to determine real world conditions, and the data is then on-chained and fed to smart contracts. Through the oracle the smart contracts are able to have a window to the real world and reliably know when a climate risk occurs.

The oracle can report on various climate risks ranging from wildfires, drought, air degradation, crop failure, lack of forage etc Through the data on-chained by the oracle the parametric insurance solution can be configured to address any type of climate risk. If a risk has occurred, this triggers an automatic claims process.

Once payout is triggered, the payment can be made to the beneficiary's crypto or MPESA wallet. Based on the user preference, a payment is automatically made to the required wallet. This interoperability between web3 and local digital payment solutions allows anyone currently using a local digital payment solution such as MPESA to access Web3-based climate insurance powered by CBDCs.

How we built it

We developed smart contracts and deployed these on the Ripple EVM sidechain where CBDCs will be bridged. The smart contracts link to a web application that also links to a local payment solution in Kenya called M-PESA. When an insurance contract is deployed on-chain, it is loaded with CBDCs which upon settlement can be off-ramped to MPESA. The data oracle provides the smart contracts with information regarding climate risks allowing the application to determine whether a payout should be made or not. The whole process of risk assessment and payout is automated allowing for rapid settlement.

We also built the solution to be highly flexible. It can be used to roll out individual insurance contracts as well as group insurance contracts. This makes it highly useful for the communities in the Global South where climate resilience is built at the community level.

Integrating the crypto and fiat payments means beneficiaries do not need to be crypto or even tech-savvy to benefit from the solution.

Challenges we ran into

One of the challenges we ran into is that there is no integration between Chainlink technology that we use for the data oracle, and the Ripple EVM sidechain. We developed an integration between the two but initially faced an issue with the oracle node and the EVM sidechain RPC node falling out of sync after a certain period elapsed. Once these two nodes had desynced their communication ended leading to our application not completing its workflow.

We were able to solve this through an ingenious trick of regularly resyncing the nodes. Restarting the node forced it to resync with the network. We implemented a script on Kubernetes that periodically restarted the Chainlink node allowing it to resync with the RPC node and thereby circumventing the desyncing issue. This fixed the biggest technical challenge we encountered.

A second challenge we ran into is the fact that CBDCs are not yet available on the Ripple EVM sidechain. We expect that in the future it will be possible to bridge CBDCs from the XRPL ledger to the XRP EVM sidechain for use in applications. As such we decided to use the XRP token already available on the EVM sidechain to represent the CBDCs that will use in the future.

We also faced issues in integrating the crypto and web2 side of payments. Getting our solution to handle both payments in CBDCs (crypto) as well as in MPESA (web2) required the building of an off-ramp application connected to both web3 and MPESA payment rails. This was developed in-house to meet the requirements of the institutional users of the solution.

Accomplishments that we're proud of

We are proud to have built a solution that addresses one of the most pressing needs of our time i.e. climate resilience. This is a solution that can provide some of the most vulnerable people with climate insurance thus allowing them to survive adverse climatic risks. It provides a financial mechanism for climate adaptation.

We are also proud of the fact that our solution integrates CBDCs with local digital payments infrastructure in a complementary way. What we use CBDCs for, the local payment solutions can't handle. As such CBDCs applied in this way open up new value propositions for the existing digital payments providers such as MPESA, rather than being competitive. This means that more than 30 million MPESA users can immediately tap into using CBDCs in new financial solutions through the interoperability we've developed.

What we learned

We have learned that there are things that MPESA cannot do that CBDCs could do very well (such as being used in web3 applications). We have also learned that there are things that local digital payments are more suitable for than CBDCs at this time. An example is the last mile of payments to non-tech-savvy users. Our biggest insight is how the integration of CBDCs and local digital payments technology can create new value which neither could achieve on its own. We believe that exploring interoperability between CBDCs and existing local digital payments is the gateway to mass adoption of CBDCs in the Global South. The development of hybrid solutions that require both web3 and web2 components to drive real-world use cases such as insurance is one of the ways to mainstream CBDCs.

Our solution also positions CBDCs at the center of climate change discussions which for the Global South majorly revolve around climate change adaptation. As the world heads into COP28 the demand for financial mechanisms to support loss and damage financing is growing. This financing is projected to hit $300 billion per year for developing countries by 2030. Our solution provides the technology framework through which climate adaptation funds can be channeled reliably and scalably to the grassroots. It is one of the most compelling use cases for Central Banks in countries like Kenya which are discussing the potential of CBDCs and at the same time are strategically positioning themselves to lead in climate adaptation.

What's next for BlockBima

Security, Marketing, and Fundraising.

We will follow up with taking the BlockBima solution through a security audit of its smart contracts and web applications. As this is done and all loose ends are being tied, we will begin marketing the solution to corporates like banks and insurance companies who can use it to launch new insurance products. We also plan to market it to micro-finance and micro-insurance firms looking to innovate new forms of climate insurance, especially for the pastoralists and smallholder farmers that form their customer base. We will also be fundraising to raise the resources needed to launch and build out the business.

Built With

- geospatial-data

- machine-learning

- python

- react

- ripple

- solidity

Log in or sign up for Devpost to join the conversation.