-

-

Landing Page

-

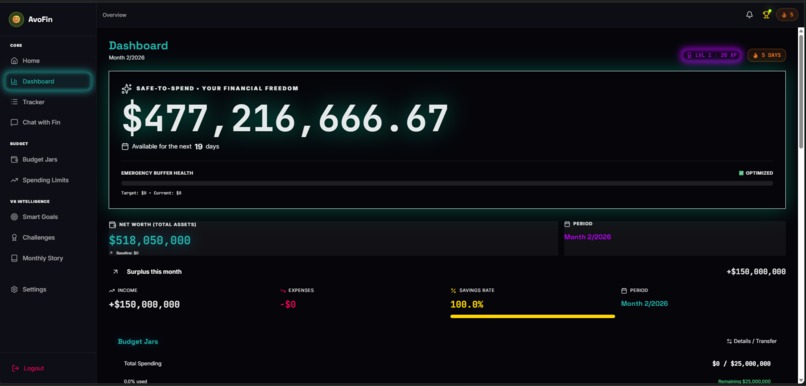

Dashboards

-

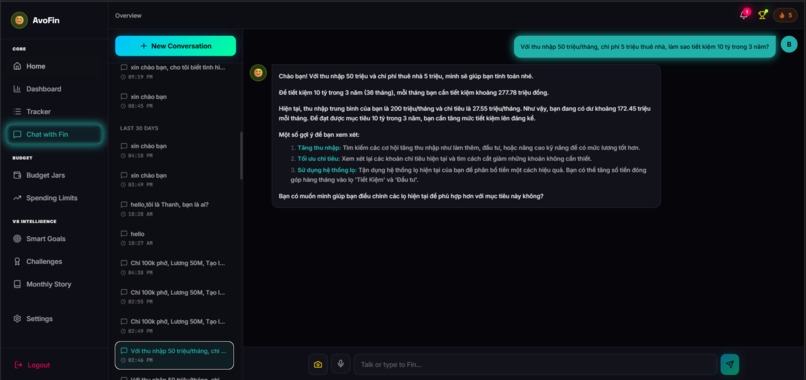

Chat with Fin

-

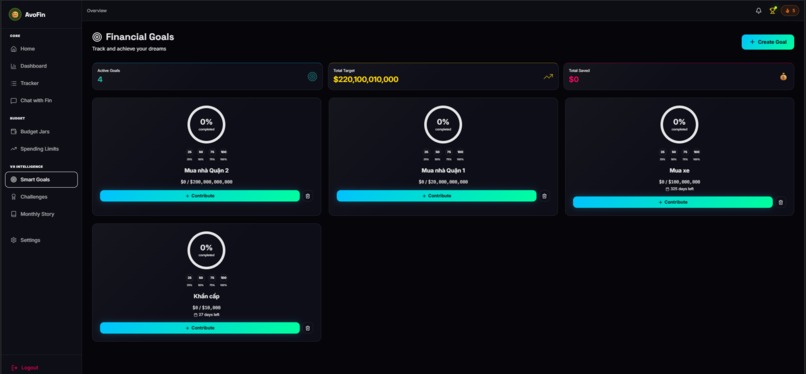

Smart Goals

-

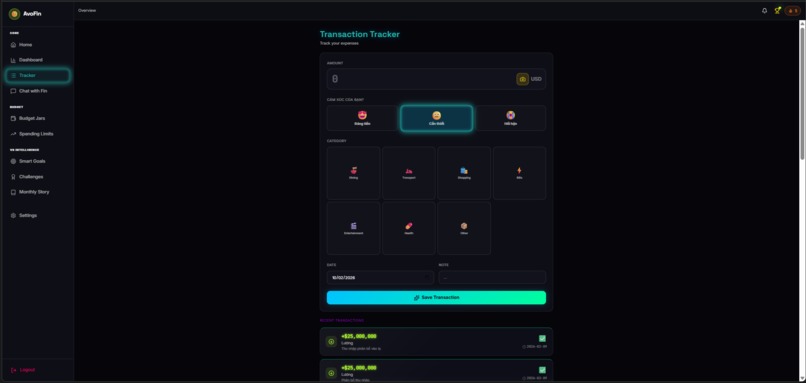

Transactions Tracker

-

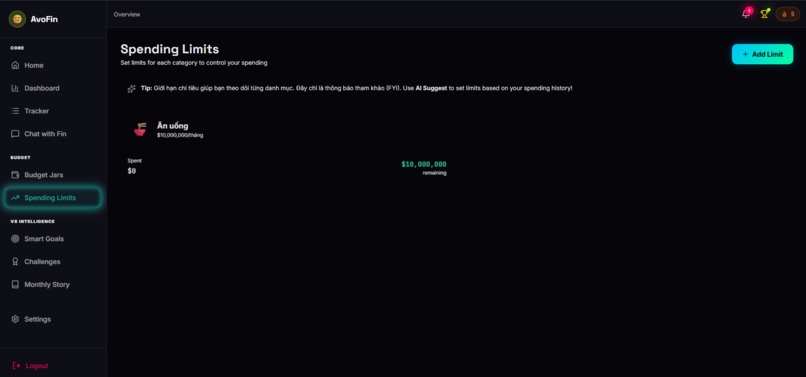

Spending Limits

-

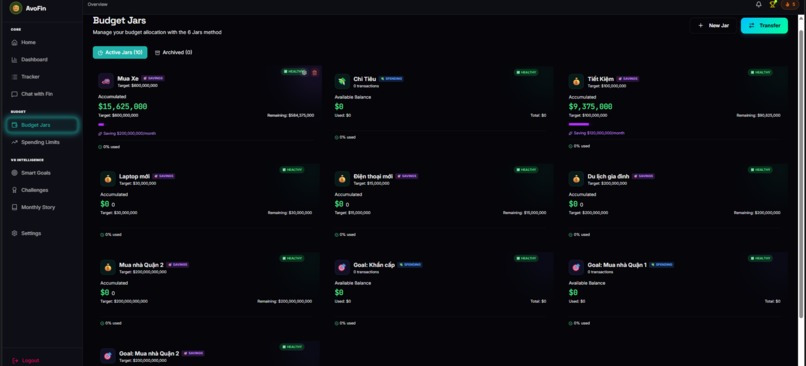

Budget Jars

-

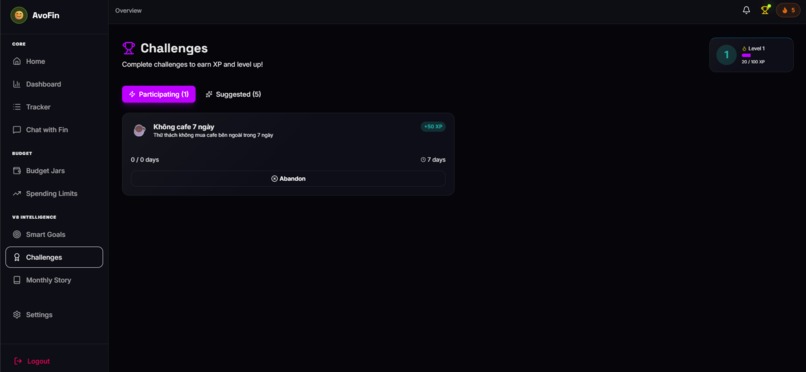

Challenge

Personal AI Finance Coaching (Cash-Flow First)

Tagline: Achieve your financial goals—without over-restricting your lifestyle.

1) Inspiration

Many people don’t struggle because they lack income—they struggle because they lack cash-flow visibility. They know how much they make, but not what’s “safe to spend” today, whether upcoming bills will create a tight week, or where small daily habits quietly drain their budget.

Most finance apps stop at logging and charts. I wanted a proactive AI Coach that helps users stay ahead of surprises and build toward financial freedom—without extreme budgeting.

2) What the product does

Personal AI Finance Coaching is a cash-flow-first AI agent. It continuously models a user’s inflows and outflows to answer the most actionable question:

“How much can I safely spend right now while still hitting my goals?”

Core features

- Cash-flow timeline: paydays, recurring bills, and projected variable spend across the month.

- Safe-to-spend guidance: adaptive daily/weekly spend limit based on time-to-payday, upcoming obligations, and goals.

- Spending leak detection: identifies “silent drifts” (e.g., coffee, delivery, subscriptions) that grow month-over-month.

- Early warnings: alerts before the user crosses risk thresholds or misses a target surplus.

- Goal-driven coaching: ties daily decisions to outcomes (monthly surplus, emergency fund, debt payoff).

3) How I built it (AI + Systems)

I built it as a hybrid system: deterministic cash-flow math for reliability, and an LLM layer for messy real-world data + coaching.

A) Cash-flow engine (deterministic)

- Builds forward-looking projections from income schedule + recurring bills + spending pace.

- Computes cash runway, bill coverage, and safe-to-spend ranges.

- Produces explainable drivers for every alert (e.g., “this changes because rent is due in 3 days”).

B) LLM pipeline for transaction understanding (Prompt Engineering)

Real transaction data is noisy (merchant aliases, ambiguous descriptions). Instead of relying only on regex, I use an LLM with:

- Few-shot prompt templates to classify transactions and normalize merchants (output constrained to a strict JSON schema).

- Tool-augmented prompts: the model calls a lightweight ruleset + merchant dictionary first, then resolves uncertain cases.

- Feedback loop: when users correct a category/merchant once, that rule is stored and reused (personal rules > global rules).

This approach improves robustness on edge cases (new merchants, localized descriptions) while keeping results predictable and auditable.

C) AI Agent for hyper-personalized coaching

The “coach” is an agent that combines:

- User habit memory (recurring patterns like “morning coffee”, payday rhythm, bill seasonality),

- Anomaly detection (spikes, new recurring charges),

- Goal planner (what needs to change this week to still hit the month-end target),

to deliver short, contextual nudges like:

- “You’re on track, but your weekday coffee spend is trending up—reduce by X for the next 4 days to keep your surplus goal.”

- “A new recurring charge appeared; if it continues, it will reduce next month’s runway by Y.”

4) Challenges (and how I solved them)

1) Noisy, inconsistent transaction data

Merchant strings vary wildly; categories are ambiguous. I tackled this with LLM-based normalization and classification using prompt engineering (few-shot + constrained JSON outputs), plus a user-feedback memory so the system becomes more accurate over time.

2) Forecasting without making users feel restricted

Rigid envelopes cause churn. I designed flexible guardrails: safe-to-spend adapts to payday timing, bill schedule, and progress toward goals—so users feel guided, not punished.

3) Trust and explainability

Financial advice must be transparent. Every alert includes the concrete driver: upcoming bills, spending pace, or new recurring charges—so users understand why the system is nudging them.

4) Avoiding notification fatigue

The agent ranks insights by impact on month-end outcome and only surfaces high-signal actions, keeping coaching lightweight and actionable.

5) Early results (choose ONE option below)

Option A — If you have a small test/pilot (recommended)

“In a small pilot with [N] users over [X] days, users reduced identified ‘wasteful spend’ by [Y]% in the first week and ended the month with an average surplus improvement of [Z].”

Option B — If you don’t have measurable results yet (safe, honest)

“During internal demos and structured test scenarios, the agent consistently caught spending leaks (e.g., new subscriptions, growing daily habits) and issued early warnings ahead of bill dates—helping users adjust spending before it became a month-end deficit.”

6) What’s next

- Stronger recurring detection (annual bills, variable subscriptions).

- Deeper personalization (habit-based safe-to-spend, context-aware coaching).

- “Why did this change?” explanations for every safe-to-spend update.

- Privacy-first processing options where possible.

Technology Stack

- Frontend & Deployment: Vercel (Next.js hosting and CI/CD)

- Backend & Database: Supabase (Postgres, Auth, Row Level Security, Storage, Edge Functions)

- AI/LLM: Google Gemini (transaction understanding, coaching generation, structured JSON outputs)

Built With

- gemini

- superbase

- vercel

Log in or sign up for Devpost to join the conversation.